Loading component...

Lynn Paulson

SVP/Director of Agribusiness Development

Lynn Paulson

SVP/Director of Agribusiness Development

6/12/2025 1:00:00 PM

In an era of fluctuating markets, shifting policies and persistent economic pressures, agricultural producers and agribusinesses are once again navigating a difficult economic environment. From the ripple effects of tariffs to the burden of deficit spending and inflation, the ag sector is forced to adapt to shifting financial realities while striving to maintain stability and growth.

Let’s dive deeper into the key challenges facing farmers, ranchers and producers today.

Agriculture, perhaps more than any other industry, is deeply intertwined with global trade. The imposition of tariffs on key exports has reshaped market dynamics, forcing producers to rethink traditional strategies. Tariffs on agricultural commodities have led to retaliatory measures from trading partners, affecting the profitability of U.S. farm products abroad. Agricultural producers are seemingly always on the front lines of these economic disruptions.

While government ad hoc disaster programs have offered temporary financial relief, the long-term sustainability of such interventions remains uncertain. Moreover, it’s unclear if the political will – or money – will be there year after year should the negative effects of tariffs continue to impact producers.

The lack of predictable trade agreements can make long-term planning difficult, requiring producers to adopt more agile financial strategies to withstand market disruptions. As much as possible, producers reliant on export markets may need to explore value-added products and seek out new trading partnerships to mitigate associated risks. This theme – of being able to call an audible for your operation when faced with uncertain conditions – is one that I’ll discuss in detail at our AgViews Live seminar in July.

The U.S. deficit is now approaching $37 trillion. In May, Moody’s downgraded the U.S. credit rating for the first time in history. Interest on the national debt is projected to be an astronomical 30% of revenue by 2035. The U.S. debt to gross domestic product (GDP) is about 122% — up from 62% in 2007. As federal spending and the debt increase, questions about long-term consequences — such as inflationary pressure, interest rate hikes and reduced government support programs — loom large for agricultural businesses.

Increased deficit spending can drive up borrowing costs, making it harder for farmers to access affordable credit for operational expenses, equipment purchases and expansion plans. Additionally, a ballooning federal deficit with large required mandatory spending leaves little money for discretionary farm programs like crop insurance and disaster relief.

Rising costs have created a significant financial strain across the country, leaving businesses with shrinking profit margins. The agricultural sector, already vulnerable to tight margins, is seeing substantial price hikes across essential inputs. The costs of fertilizer, chemicals, seed, fuel, repairs and labor are all higher. Input costs for producers have increased by about $90 billion since 2021.

Another point to consider: At the retail level, inflation impacts consumer purchasing habits, affecting demand for certain agricultural products. Higher grocery prices may shift consumer preferences toward cheaper alternatives, creating volatility for producers reliant on price-sensitive markets. For example, is it reasonable to think most consumers can continue to pay $6 per pound for ground beef?

Moreover, these macroeconomic factors will undoubtedly continue to drive consolidation at all levels, from individual farm operations to large businesses that support agriculture. For example, in banking, consolidation has led to the four largest banks in the U.S. having a whopping $11.9 trillion in assets. To put that in perspective, the 4,300 banks under $10 billion have a combined $3.4 trillion in assets. Are large banks too big to fail?

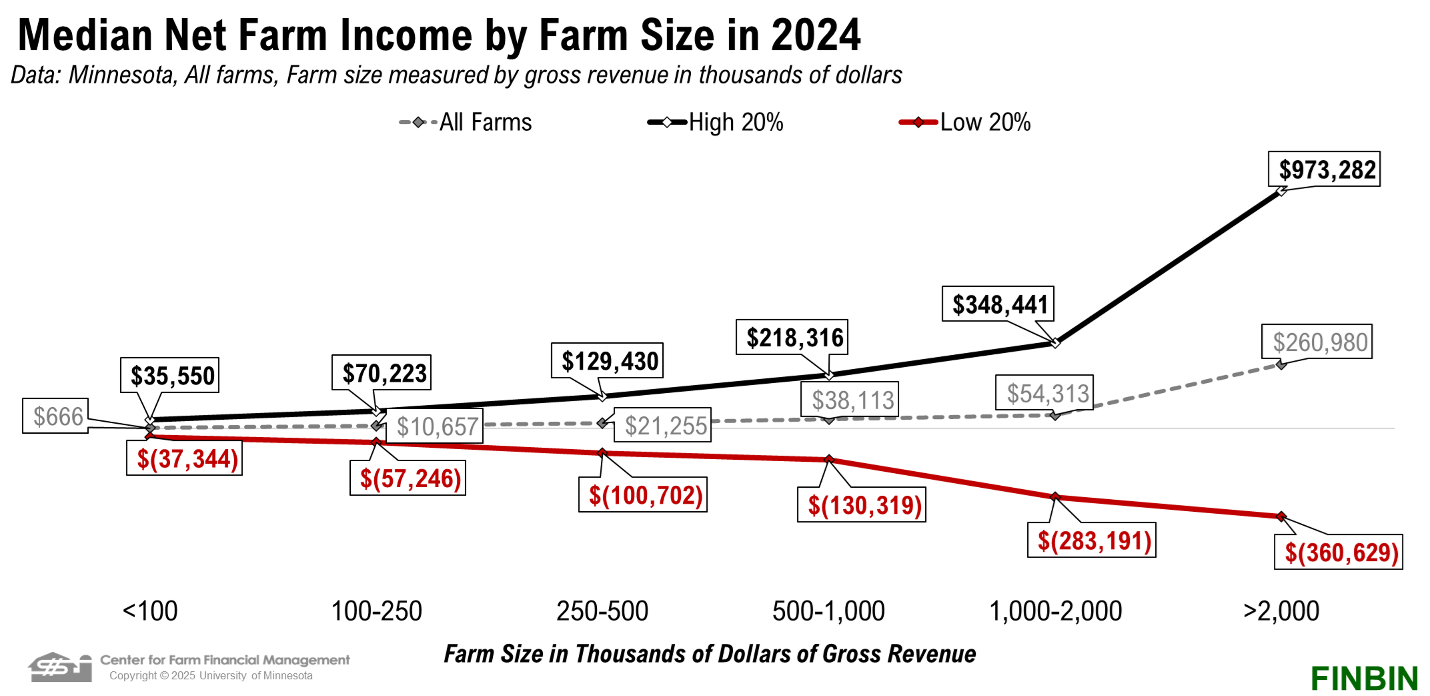

In the face of all these challenges, how did farm and ranch operations do in 2024? The Center for Farm Financial Management chart below, which shows median net farm income by farm size, gives us an idea. This data set includes producers from all ag sectors, and shows how, as operations grow larger by gross revenue, there is a wider profitability spread between the top 20% and the bottom 20%. Bigger isn’t always better. From a historical perspective, the 2024 chart is an accurate reflection of the variability in farm sector economics.

There is currently a bifurcated farm economy. Grain or row crop producers are generally feeling stressed with commodity prices down 30%-40% over the past 2-3 years, while input costs, as noted earlier, have continued to increase. On the other hand, livestock producers – especially established cow and calf producers – are mostly faring well. I noted in a previous newsletter that the steer I bought last year cost me about $4,000 (including processing). I’m guessing it will be up another $1,000 – to about $5,000 – this year.

When taking a forward-looking view, it’s hard to plan. Is it reasonable to assume we’ll have a status quo with farm policy, no ad hoc government payments, no supply shock and no change in consumer behavior? Unfortunately not. Instead, remember the “CTC” principle – control the controllables.

From an ag lender’s perspective, here are a few thoughts and observations on the state of the ag economy:

As we move forward, it will be crucial to stay informed on economic trends, embrace adaptive strategies, and foster collaboration within the industry. The future of agriculture will be shaped by those who recognize both the risks and the opportunities inherent in today’s economic landscape.

This article appeared in the Q2 2025 issue of Bell’s AgViews newsletter.